Forecast process

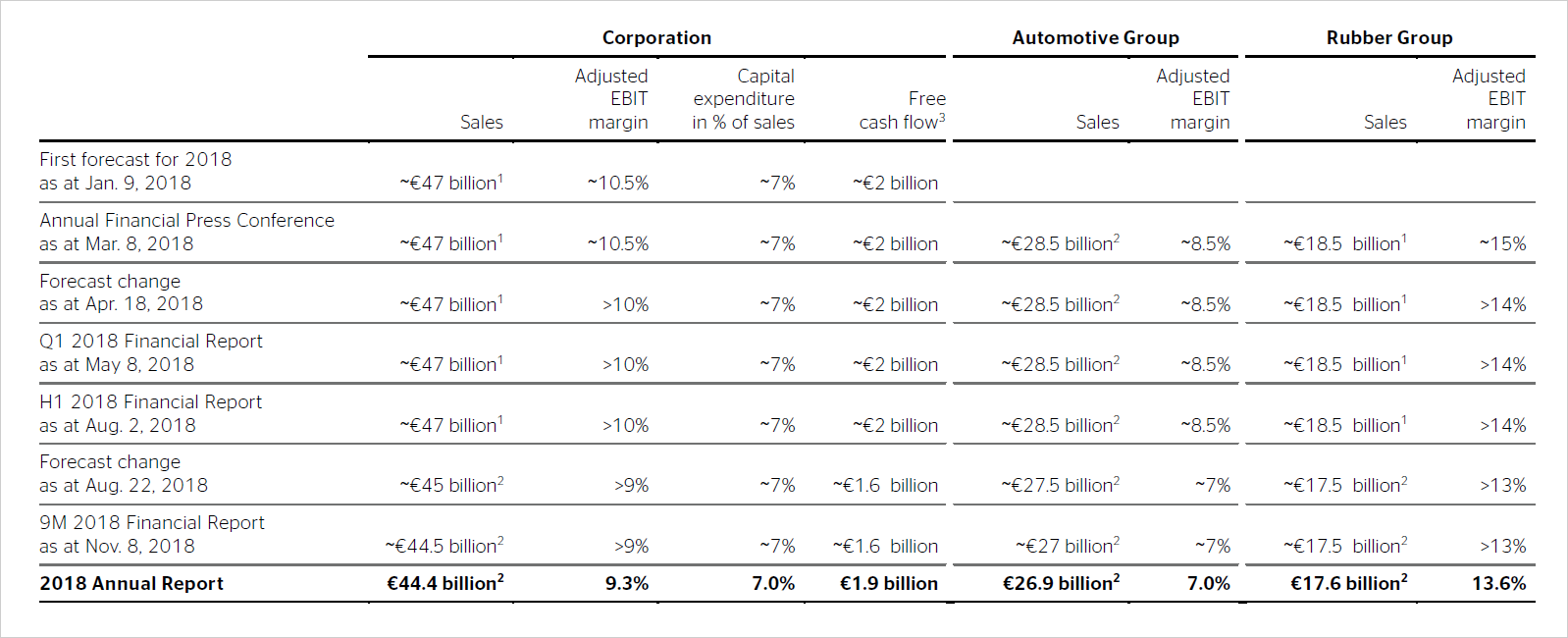

In January, Continental already reports its initial expectations regarding the most important production and sales markets for the new fiscal year. This forms the basis of our forecast for the corporation’s key performance indicators, which we publish at the same time. These include sales and the adjusted EBIT margin for the corporation. In addition, we provide information on the assessment of important factors influencing EBIT. These include the expected negative or positive effect of the estimated development of raw materials prices for the current year, the expected development of special effects and the amount of amortization from purchase price allocation. We thus allow investors, analysts and other interested parties to estimate the corporation’s expected EBIT. Furthermore, we publish an assessment of the development of interest income and expenses as well as the tax rate for the corporation, which in turn allows the corporation’s expected net income to be estimated. We also publish a forecast of the capital expenditures planned for the current year and the free cash flow before acquisitions and certain exceptional effects, if any.

When we prepare the annual report, we supplement this forecast for the corporation with a forecast of the sales and adjusted EBIT margins of the two core business areas: the Automotive Group and the Rubber Group. We then publish this forecast in March as part of our annual financial press conference and the publication of our annual report for the previous year.

The forecast for the current year is reviewed continually. Possible changes to the forecast are described at the latest in the financial report for the respective quarter. At the start of the subsequent year, i.e. when the annual report for the previous fiscal year is prepared, a comparison is made with the forecast published in the annual report for the year before.

In 2015, Continental compiled a medium-term forecast in addition to the targets for the current year. This comprises the corporate strategy, the incoming orders in the Automotive Group and the medium-term targets of the Rubber Group. Accordingly, we want to generate sales of more than €50 billion in the medium term. This could be achievable as early as 2020 depending on customer market trends, but equally may not be attainable until after 2020 on account of the current difficult market conditions and volatile exchange-rate parities. We are aiming for a return on capital employed (ROCE) of at least 20% in the long term. These targets were also confirmed after the review in 2018.

Comparison of the past fiscal year against forecast

Unfortunately, we failed to meet our forecast for fiscal 2018, which we had published in full in March 2018, with respect to sales and adjusted EBIT margin. Instead of the planned sales figure of around €47 billion, assuming exchange rates remain constant year-on-year, the Continental Corporation achieved sales of €44.4 billion. The corporation was aiming for an adjusted EBIT margin in the region of 10.5%, but the actual figure was 9.3%.

On April 18, 2018, we lowered the earnings forecast for the Rubber Group from approximately 15% to more than 14% for 2018 due to exchange-rate and inventory-valuation effects, which impacted the Rubber Group’s earnings in the first half of 2018. For the corporation, this also resulted in the forecast for the adjusted EBIT margin being lowered from around 10.5% to more than 10%. All other aspects of the forecast remained the same. We maintained the changed forecast in the first-quarter reporting in May 2018 and again in the reporting on the first half of the year in August 2018.

1 Assuming exchange rates remain constant year-on-year.

2 Reported sales including exchange-rate effects. The negative exchange-rate effects for the corporation amounted to €1.1 billion in 2018. Around half of this was attributable to

the Automotive Group, and the other half to the Rubber Group.

3 Before acquisitions and before the net outflow for the funding of the U.S. pension plans in 2018.

On August 22, 2018, lower sales expectations, cost increases and warranty cases forced us to announce another change to our forecast. The main reasons for this were the decline in original equipment business in the major sales markets of Europe and China during the second half of 2018 and weak demand in the tire market in these regions. This was exacerbated by higher-than-anticipated development costs in the Automotive Group as a result of high incoming orders and start-up costs for new products and plants.

The forecast for consolidated sales in 2018 – including negative exchange-rate effects – was reduced to around €45 billion, while the forecast for the corporation’s adjusted EBIT margin was lowered to more than 9%. The guidance for the Automotive Group’s sales – including negative exchange-rate effects – was reduced to around €27.5 billion with an adjusted EBIT margin of around 7%. The sales forecast for the Rubber Group – including negative exchange-rate effects – was lowered to around €17.5 billion and the adjusted EBIT margin was revised to more than 13%. The guidance for free cash flow before acquisitions and before the net outflow for the funding of the U.S. pension plans was reduced to approximately €1.6 billion for the current year. Almost all aspects of the revised forecast were confirmed in November 2018 in the reporting on the first nine months of the year. The corporation’s sales guidance was the only aspect to be lowered slightly to around €44.5 billion due to weaker development in China.

Continental achieved consolidated sales of €44.4 billion and a consolidated adjusted EBIT margin of 9.3% in fiscal 2018. The Automotive Group generated sales of €26.9 billion and an adjusted EBIT margin of 7.0%. The Rubber Group generated sales of €17.6 billion and an adjusted EBIT margin of 13.6%.

The negative financial result decreased to €177.8 million in 2018, which was in line with our expectations. In January 2018, we had forecast a negative financial result of less than €190 million before effects from currency translation, effects from changes in the fair value of derivative instruments, and other valuation effects. In March 2018, we lowered this forecast to less than €180 million.

The tax rate for fiscal 2018 went down to 23.2%. In January 2018, like at the start of the previous year, we had assumed a figure of less than 30%. In the reporting on the first half of the year in August, we lowered this figure to around 25%. This was due primarily to the effects of the tax reform in the U.S. and to tax refunds for previous years on the back of a supreme court ruling in Germany. In November, we slightly adjusted our guidance for the tax rate to around 24%.

The capital expenditure ratio increased to 7.0% in 2018, as had been forecast in January 2018. Free cash flow before acquisitions and before the net outflow for the funding of the U.S. pension plans amounted to €1.9 billion in 2018, a figure between the guidance of January 9, 2018, and the lowered forecast of August 22, 2018.

Order situation

The order situation in the Automotive Group was extremely positive in the past fiscal year, as it was in the previous year. As such, incoming orders for the three Automotive divisions remained on par with the previous year’s record level. Altogether, the Chassis & Safety, Powertrain and Interior divisions again acquired orders for a total value of roughly €40 billion for the entire duration of the deliveries. These lifetime sales are based primarily on assumptions regarding production volumes of the respective vehicle or engine platforms, the agreed cost reductions and the development of key raw materials prices. The volume of orders calculated in this way represents a reference point for the resultant sales achievable in the medium term that may, however, be subject to deviations if these factors change. Should the assumptions prove to be accurate, the lifetime sales are a good indicator for the sales volumes that can be achieved in the Automotive Group in four to five years.

The replacement tire business accounts for a large portion of the Tire division’s sales, which is why it is not possible to calculate a reliable figure for order volumes. The same applies to the ContiTech division, which since January 2018 has comprised seven business units operating in various markets and industrial sectors, each in turn with their own relevant factors. Consolidating the order figures from the various ContiTech business units would thus be meaningful only to a limited extent.

Outlook for fiscal 2019

For fiscal 2019, we currently anticipate that global production of passenger cars and light commercial vehicles will be at roughly the same level as the previous year. The declining market performance we experienced over the second half of last year looks set to continue unabated in the first half of 2019. For the second half of the year, we anticipate slight increases in production compared with the low prior-year basis. The positive trend in demand for replacement tires for passenger cars and light commercial vehicles is expected to continue in all regions in 2019. On a global level, we expect it to increase by 2%.

Based on these market assumptions and in light of what continues to be a highly volatile market environment – and provided that exchange rates remain constant – we anticipate total sales of between around €45 billion and €47 billion and an adjusted EBIT margin of approximately 8% to 9% in fiscal 2019.

For the Automotive Group, assuming constant exchange rates, we anticipate sales of approximately €27 billion to €28 billion with an adjusted EBIT margin of around 6% to 7%. For the Rubber Group, assuming constant exchange rates, we anticipate sales of approximately €18 billion to €19 billion with an adjusted EBIT margin of around 12% to 13%.

For the Rubber Group, we anticipate increased fixed costs in the Tire division in 2019. This increase in fixed costs has resulted primarily from the considerable expansion of capacity over recent years. The utilization of the new capacity and the generation of related sales will not positively impact the cost situation until 2020 onwards.

If demand for tires increases worldwide over the course of the year, as we expect it to, this is likely to be reflected in rubber prices at a commensurately fast rate. We are anticipating an average price of U.S. $1.46 per kilogram (2018: U.S. $1.36 per kilogram) for natural rubber (TSR 20) and U.S. $1.43 per kilogram (2018: U.S. $1.41 per kilogram) for butadiene, a base material for synthetic rubber. Moreover, we expect the import tariffs that have been levied by various countries to increase the costs of steel cord. We do not expect the recent resurgent price of crude oil to produce a positive impact on the cost of carbon black and other chemicals year-on-year. Generally speaking, every U.S. $10 increase in the average price of crude oil equates to a negative gross effect of around U.S. $50 million on the Rubber Group’s operating earnings. Overall, we expect rising raw material prices to have a negative effect of approximately €50 million on the Rubber Group in 2019.

In 2019, we expect the negative financial result before effects from currency translation, effects from changes in the fair value of derivative instruments, and other valuation effects to be in the region of €220 million. The fact that this figure is higher than in the previous year can be attributed primarily to the new standard IFRS 16, Leases, which has to be applied starting in the 2019 fiscal year. It stipulates that interest expenses resulting from the measurement of lease liabilities are to be reported in the financial result.

The tax rate – including the tax effects from the transformation of the Powertrain division into an independent group of legal entities – is expected to be around 27% in 2019.

For 2019, taking into account expenses relating to the transformation of the Powertrain division into an independent group of legal entities, we expect negative special effects to total €200 million.

Amortization from purchase price allocations, resulting primarily from the acquisitions of Veyance Technologies (acquired in 2015), Elektrobit Automotive (acquired in 2015) and the Hornschuch Group (acquired in 2017), is expected to total approximately €200 million and to affect mainly the ContiTech and Interior divisions.

In fiscal 2019, the capital expenditure ratio before financial investments will increase to around 8% of sales. This increase is chiefly attributable to the recognition of leases as a result of the first-time adoption of IFRS 16. Approximately 60% of capital expenditure will be attributable to the Automotive Group and 40% to the Rubber Group.

The largest projects within the Chassis & Safety division in 2019 remain the global expansion of production capacity for the new generations of electronic brake systems in the Vehicle Dynamics business unit. Further extensive capital expenditure is planned for the global expansion of production capacity for sensors. The Powertrain division will continue its investments in a new plant in China. Investments in the Hybrid Electric Vehicle business unit are also a priority for capital expenditure. The Interior division is continuing to invest in the construction of new plants in Eastern Europe, North America and China and in the industrialization of new display technologies in 2019.

This year, like last year, investments in the Tire division will focus on the expansion of passenger tire production in Asia, North America, and Southern and Eastern Europe. In the area of commercial-vehicle tires, the emphasis will be on the expansion of production capacity in North America and Eastern Europe. In 2019, the ContiTech division will be directing its investments toward expanding production in the Benecke-Hornschuch Surface Group business unit in Asia, predominantly in China and India.

As at the end of 2018, Continental’s net indebtedness amounted to €1.7 billion. The first-time adoption of IFRS 16, Leases, will approximately double net indebtedness as at January 1, 2019. In the future, we intend to continue strengthening the industrial business in particular, in line with our objective of reducing our dependency on the automotive original equipment sector. The acquisition of further companies for this purpose has not been ruled out. Another focus will be the selective reinforcement of our technological expertise in future-oriented fields within the Automotive Group.

In 2019, we are planning on free cash flow of approximately €1.4 billion to €1.6 billion, before acquisitions and before the effects of transforming the Powertrain division into an independent group of legal entities. This year-on-year decline is due mainly to the market environment on an operational level. We also expect a portion of the warranty provisions recognized in 2018 to flow out.

The start to 2019 has so far confirmed our forecast for the full year. As anticipated, market conditions are proving very challenging – particularly in China but also in Europe.