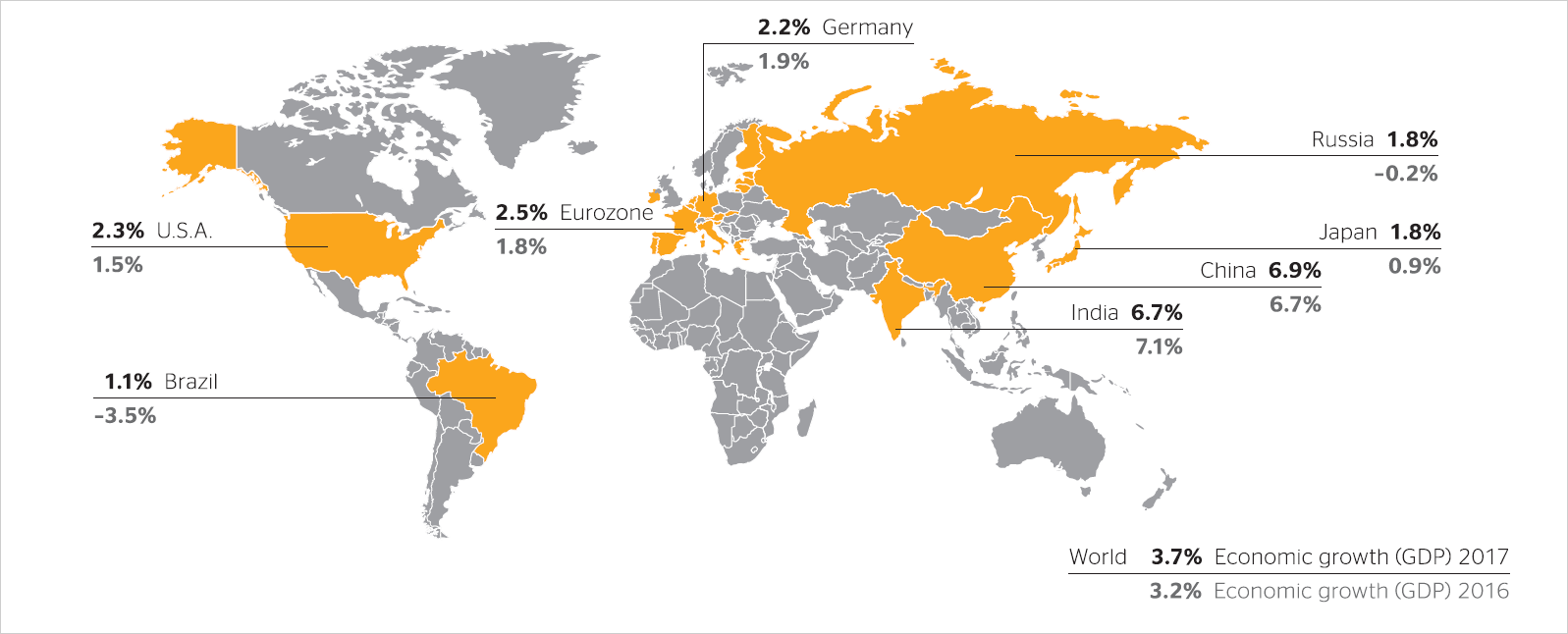

In Germany, the solid economic growth of recent years accelerated in 2017. According to initial calculations by the German Federal Statistical Office, gross domestic product (GDP) increased by 2.2% year-on-year when adjusted for prices in the year under review, after 1.7% in 2015 and 1.9% in 2016. This clearly surpassed the forecast of 1.5% formulated by the International Monetary Fund (IMF) in January 2017. The significant growth was due in particular to higher private investment, but also consumer and public spending.

In addition to Germany, the other countries of the eurozone also saw a continuing economic upturn in 2017 for the most part thanks to higher capital expenditure by companies and increased consumer and public spending. According to the latest figures from the statistical agency Eurostat, the eurozone economy achieved GDP growth of 2.5% in the year under review and likewise surpassed the IMF forecast of 1.6% from January 2017. Economic development was boosted further by the monetary policy of the European Central Bank (ECB), which continued to adhere to its expansionary measures in 2017.

The U.S. economy picked up momentum from quarter to quarter during 2017 and is expected to have achieved GDP growth of 2.3%, meeting the IMF’s forecast from January 2017 precisely. This was due primarily to an increase in consumer spending and private investment. In March, June and December 2017, the U.S. Federal Reserve (Fed) increased its key interest rate by 25 basis points each time. With a most recent target of between 1.25% and 1.5%, its key interest rate nevertheless remained low.

The Japanese economy recovered in the year under review, thanks especially to the sharp increase in the foreign trade surplus due to the weakening of the Japanese yen against the euro and other currencies. Private investment and consumer spending also increased, while government spending virtually stagnated. Based on the IMF’s current expectations, the Japanese economy may have grown 1.8% year-on-year in 2017, partly due to the continuing expansionary monetary policy of its central bank. The growth was therefore much stronger than the 0.8% forecast by the IMF at the start of the year.

According to the IMF’s WEO Update (World Economic Outlook, WEO) from January 2018, emerging and developing economies achieved growth totaling 4.7% in 2017 (PY: 4.4%). In January 2017, the IMF had initially forecast 4.5%. China and India were the main growth drivers once again. With a reported increase in GDP of 6.9%, the Chinese economy performed better than the IMF’s forecast of 6.5% at the start of 2017. By contrast, the IMF reports that India’s GDP grew by 6.7%, falling short of its forecast of 7.2% because the radical reform of the VAT system had a dampening effect on the economy. Russia and Brazil also performed better in the reporting year than expected in January 2017, benefiting from the recovery of the raw-materials sector.

The IMF’s January 2018 WEO Update indicates that the global economy grew by 3.7% after 3.2% in the previous year. The IMF’s January 2017 forecast of 3.4% growth was surpassed as a result of the stronger economic performance in the eurozone as well as in Japan and China.

Year-on-year economic growth (GDP) in 2017

Sources: IMF – World Economic Outlook Update January 2018, Eurostat, statistical offices of the respective countries, Bloomberg.