General Disclosures (ESRS 2)

Notes on Applying the ESRS

General basis for preparation of the sustainability report

This report was prepared in accordance with the European Sustainability Reporting Standards (ESRS).

For the preparation of this report and based on the set of formal and content requirements, internal experts were identified for quantitative disclosures and qualitative disclosures. The content of the sustainability report was prepared by the relevant experts and then consolidated and reviewed by the Group Sustainability group function. The report was formally approved as part of the overall financial reporting process. Operational supervision lies with the Sustainability Steering Committee, whose members include the entire Executive Board of the Continental Group. Sustainability reporting also falls under the supervision of the Supervisory Board. Further information on supervision can be found in the Consideration of sustainability matters in corporate supervision subsection.

The reported metrics are based on specific definitions, assumptions and calculation models. It should be noted that metrics based on models or extrapolations, such as Scope 3 GHG emissions or substances of concern, are subject to uncertainties. Where relevant, these uncertainties are stated directly with the respective metric under definitions, assumptions and calculation methods.

The statement in accordance with ESRS 2.77 that metrics are not subject to validation by an external body other than the independent auditor has not been repeated for each metric, as this applies to all metrics.

When applying the ESRS, the terminology of the ESRS is used as a general rule while also taking into account terminology comprehensibility and consistency within the management report as well as any existing and potential further adjustments to the ESRS. For example, the section headlines used include “emissions and substances” instead of “pollution,” while the terms used include “management approach” instead of “policy,” “key actions for target achievement” instead of “actions and resources” and “phase-in disclosure requirements” instead of “transitional provisions”.

Continental also points out some ongoing general uncertainties with regard to the application and interpretation of the ESRS.

Scope of consolidation

The sustainability report has been created on a consolidated basis for the entire Continental Group.

For the purpose of this report, Continental generally includes Continental AG as well as all subsidiaries (together referred to as Continental or the Continental Group) as of December 31, 2025, along with the impacts, risks and opportunities associated with them. The sustainability report therefore takes account of the scope of consolidation as of December 31, 2025 (see Note 4 of the Notes to the Consolidated Financial Statements). Changes in the scope of consolidation compared with the previous year are also outlined in Note 4 and additionally in Note 5 of the Notes to the Consolidated Financial Statements.

The former Automotive and Contract Manufacturing group sectors were spun off in the reporting year. The spin-off became effective upon registration in the commercial registers of Continental AG and AUMOVIO SE on September 17, 2025. AUMOVIO SE was admitted to trading on the Frankfurt Stock Exchange on September 18, 2025. Since then, subsidiaries of Continental AG that were directly or indirectly part of the spin-off are no longer part of the Continental Group.

In this sustainability report, discontinued operations of the former Automotive and Contract Manufacturing group sectors are therefore, in line with the scope of consolidation as of December 31, 2025, not included in the assessment of material impacts, risks and opportunities, nor in the management approaches or metrics for fiscal 2025. As a result, the scope of consolidation for fiscal 2025 differs significantly from that of the previous year. Selected quantitative information at group sector level is provided at the end of the sustainability report to facilitate reconciliation with the new group structure (see the “Selected Sustainability Metrics by Group Sector” table on pages 209 and 210). For information on the operations of the former Automotive and Contract Manufacturing group sectors, please refer to AUMOVIO SE’s reporting. This approach is broadly consistent with the methodology applied in the management report and enables users of the report to focus on continuing operations.

All disclosures in this report relate to the fiscal year from January 1 to December 31, 2025. Where relevant, information up until the actual publication of this report has been considered. An overview of the relevant data points that derive from other European legislation and where they can be found in this sustainability report is included in the Overviews and Index Tables section (starting on page 215).

Changes to the preparation and presentation of sustainability information

Applying the principle of “materiality of information” and the assessment of significance, information on the following metrics was omitted in the reporting year compared with the previous year:

- Biogenic direct and indirect CO2 emissions

- Total used GHG removals from climate-change-mitigation projects within the Net|Zero|Now program

- Scope 3 GHG emissions

- 7. Employee commuting

- 8. Upstream leased assets

- 9. Downstream transportation

- 10. Processing of sold products

- 13. Downstream leased assets

- 14. Franchises

- 15. Investments

Significant effects also arose in the reporting year due to the spin-off of the former Automotive and Contract Manufacturing group sectors. This major organizational change must be taken into account when comparing the reported sustainability information with the previous year. As a result of the spin-off, the following metrics were omitted due to their lack of relevance to Continental’s business model:

- Allocated business with zero-tailpipe-emission vehicles

- Energy management system certifications (ISO 50001)

The processes introduced in the previous year for preparing and presenting sustainability information pursuant to the ESRS were generally retained in the reporting year, with adjustments made only where necessary and feasible in light of organizational changes.

Use was again made in the reporting year of the simplified value chain disclosure requirements pursuant to ESRS 1.132. Continental is working on being able to report these disclosure requirements in accordance with the specified time horizons in the future.

In addition, for fiscal 2025, Continental made full use of the options provided by Delegated Regulation (EU) 2025/1416 (known as the “quick fix”). These include deferring the application of phase-in disclosures and exercising the option of reduced reporting in the following topic-related sections:

- Biodiversity and Ecosystems (ESRS E4)

- Workers in the Value Chain (ESRS S2)

- Affected Communities (ESRS S3)

- Consumers and End-Users (ESRS S4)

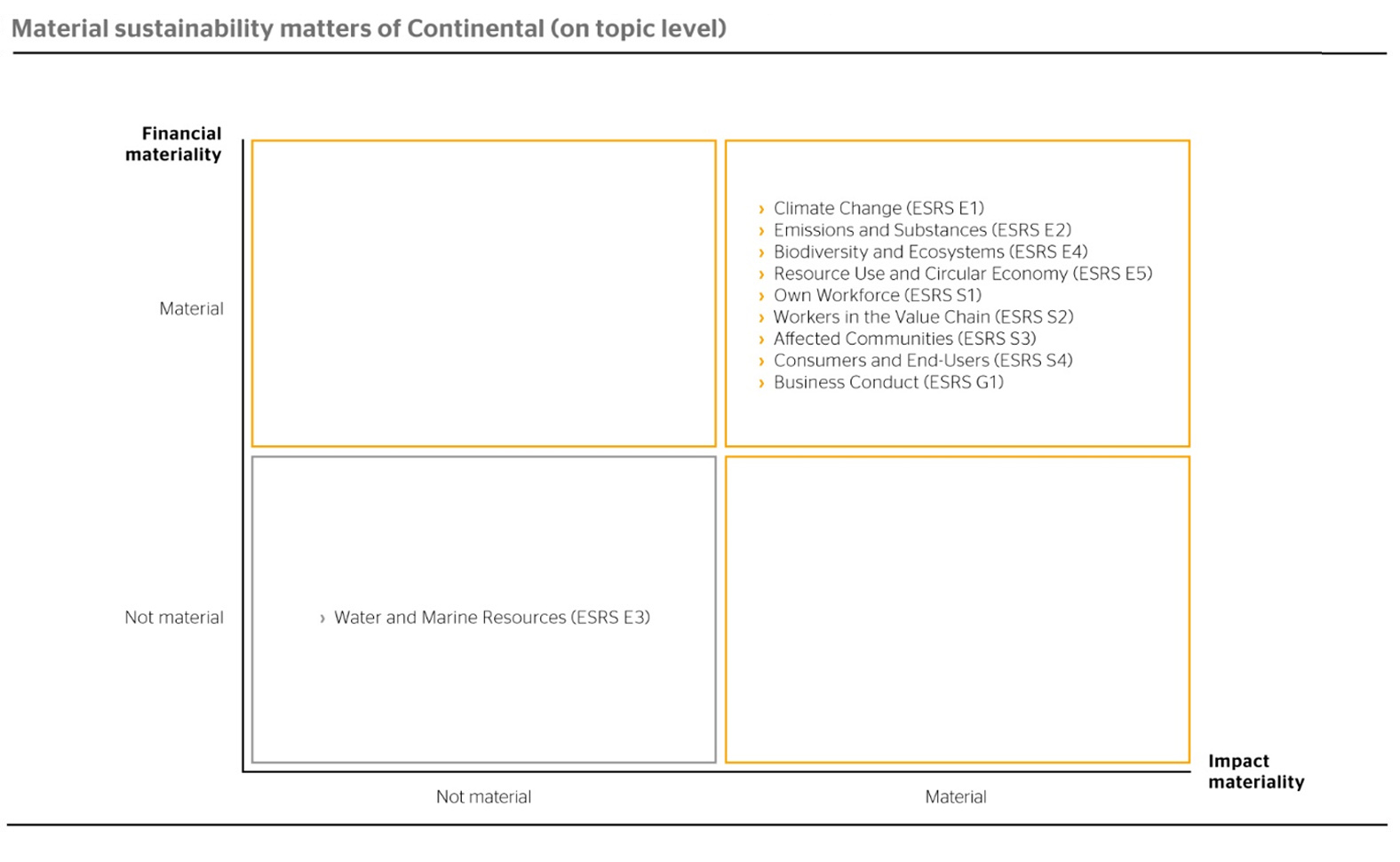

In these areas, Continental identified material impacts, risks and opportunities for the reporting year, which are listed in the table starting on page 106.

Upstream and downstream value chain

Continental’s upstream value chain includes, in particular, direct and indirect suppliers of materials and semi-finished products, such as natural rubber, synthetic rubber, other polymers, chemicals and steel. Continental’s downstream value chain includes, in particular, direct and indirect customers (e.g. vehicle manufacturers, trading companies and industrial companies), end-users (primarily vehicle users) and the treatment of products at the end of their use phase.

Continental’s upstream and downstream value chain have been included in the preparation of the sustainability report and the assessment of impacts, risks and opportunities. This includes, in particular, the consideration of supply chains (see, for example, impact ID 22 Pollution by the supply chain) and the product use phase (see, for example, impact ID 14 Pollution in the use phase). The material impacts, risks and opportunities for Continental resulting from the materiality assessment in relation to the value chain are presented in the Details of Material Impacts, Risks and Opportunities subsection and described in the topic-related sections, including the respective management approaches.

Omissions

Continental has not omitted any specific information relating to intellectual property, know-how or the results of innovation.

Continental has not made use of the exemption provided for in Article 19a (3) and Article 29a (3) of Directive 2013/34/EU or Section 289e HGB in conjunction with Section 315c (3) HGB for the disclosure of imminent developments or ongoing negotiations.

Information on targets and key actions

Continental has defined a systematic process for setting sustainability targets, taking into account the identified material sustainability-related impacts, risks and opportunities. As part of this process, two of Continental’s three time-bound sustainability targets were updated in the reporting year as a result of the group-wide transformation and redefined as follows:

- Reduce Scope 1 and market-based Scope 2 GHG emissions related to production in the tire business to an intensity of 0.13 tCO2e per tonne by 2035.

- The share of women in management positions should match with the share of women among Continental’s non-manual workers by 2030 at the latest (excluding management positions and employees in the USA).

The third target remained unchanged:

- Increase the share of recycled and renewable production materials for tires to at least 40% by 2030.

Further details on these sustainability targets and their key actions can be found in the Climate Change (ESRS E1), Resource Use and Circular Economy (ESRS E5) and Own Workforce (ESRS S1) sections. Beyond these three targets, Continental has decided to pursue the management approaches described in the respective topic-related sections without setting additional time-bound sustainability targets. The monitoring of effectiveness of the management approaches and of the progress are described in the relevant sections, including the reported metrics.

In Continental’s view, key actions to be reported relate directly to corresponding targets, where existing. Therefore, in accordance with this definition, Continental has not defined any key actions beyond the described management approaches for further sustainability topics and provides in this sustainability report only information on the key actions for the three sustainability targets specified above.

Disclosures due to other legislation on sustainability reporting

This sustainability report also constitutes the combined non-financial statement in accordance with Sections 289b to 289e and 315b and 315c in conjunction with Sections 289b to 289e HGB for the Continental Group and Continental AG for fiscal 2025. Relevant information that goes beyond the ESRS disclosures can be found in the Combined Non-Financial Statement section at the beginning of the sustainability report.

Overview of Material impacts, Risks and Opportunities

In the reporting year, Continental once again identified and assessed the material actual and potential negative and positive impacts, risks and opportunities (IROs). The detailed results are described in the Details of material impacts, risks and opportunities subsection as well as in the respective topic-related sections. The methodology of the assessment is further described in the Processes to identify and assess material IROs subsection.

The integration of impacts, risks and opportunities into the strategy and the business model is carried out in accordance with the governance processes and management approaches described in the Governance subsection and in the respective topic-related sections.

Processes to Identify and Assess Material IROs

Description of methodology and assumptions

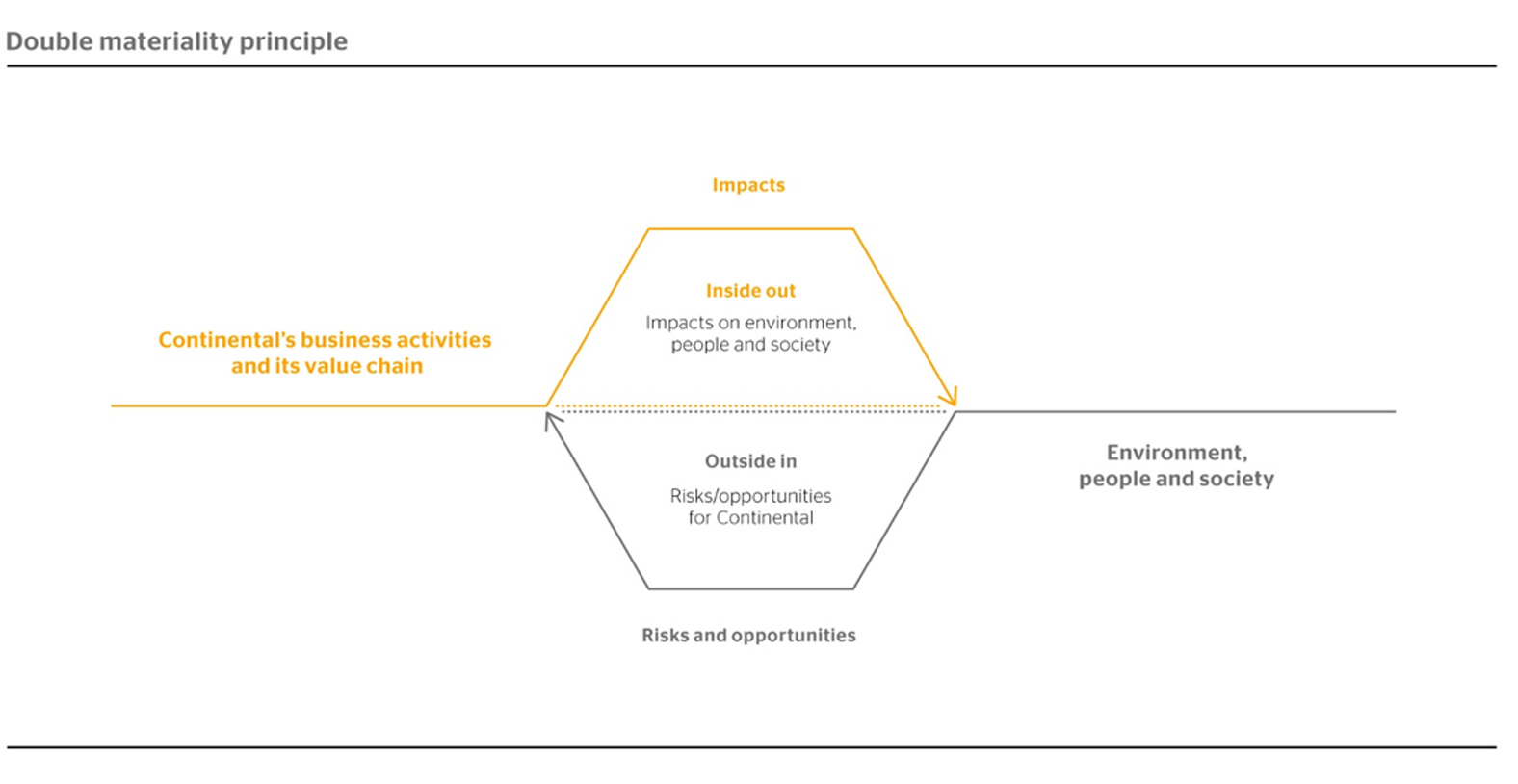

Continental assesses its impacts, risks and opportunities according to the ESRS methodology requirements on double materiality (IRO assessment). Continental’s IRO assessment was conducted simultaneously from both impact materiality (inside-out) and financial materiality (outside-in) perspectives. This approach considers abstract, business-inherent scenarios as well as tangible, company-specific scenarios, as outlined in the description of materiality dimensions. The analysis for fiscal 2025 builds on the initial assessments of fiscal 2024.

Review and adjustment of methodology and IRO longlist

The starting point for the 2025 IRO assessment was the longlist of scenarios to be evaluated compiled in the previous fiscal year, i.e. self-contained descriptions of possible situations or developments based on assumptions about relevant influencing factors, along with their associated impacts, risks and opportunities. This longlist is derived from the sustainability matters outlined in ESRS 1 AR 16 and forms the starting point for the identification of impacts, risks and opportunities. In addition, certain event types, such as sanctions, loss of sales or growth of sales, were considered for risks and opportunities. Company-specific matters were also taken into account in the identification, all of which could be assigned to the predefined list of sustainability matters. Where relevant, scenarios were broken down into those relating to own operations and those relating to the upstream and/or downstream value chain.

The initial scenarios and associated descriptions of IROs were reviewed for fiscal 2025 at topic, sub-topic or sub-sub-topic level and were aggregated or disaggregated whenever it was relevant and appropriate considering Continental’s business activities, value chain, geographical context, industries and business models. Overall, the methodology from fiscal 2024 was retained and further refined in certain aspects.

Review and update of assessments

In a first step, the IROs and their assessments were reviewed centrally and updated where necessary. This process took into consideration especially the following:

- Effects of structural changes compared with the previous year (primarily the spin-off of the former Automotive and Contract Manufacturing group sectors in the reporting year)

- Dependencies on the availability of natural, human and social resources at appropriate prices and in adequate quality, independent of the possible impacts on those resources

- Sectors and/or geographical locations, where relevant

- External studies and other scientific evidence

- External data (e.g. country risk analyses and industry risk analyses)

- Benchmark analyses

- Specific data for Continental or Continental’s value chain (e.g. Scope 3 greenhouse gas emissions)

Validation by topic experts

In a second step, the assessments based on the compiled information were reviewed by topic experts within the group. For that, employees from various Continental functions acted as representatives for internal and external affected stakeholders and/or users of sustainability information. The review included validation, updates and/or expansion of the longlist.

Determination of materiality

An iterative approach was used to document adjustments to the IRO longlist by Group Sustainability in close coordination with Group Risk Management.

The materiality threshold applied remained unchanged from the previous year. On the one hand, materiality was applied to an abstract, business-inherent assessment perspective, outlining general impact potentials and risk exposures based on structural aspects such as business activities, geographical aspects, business model and product characteristics. On the other hand, materiality was applied to a tangible, company-specific assessment perspective, taking into account the management approach, capturing residual actual negative impacts and tangible risk exposures as well as resulting positive impacts and opportunities. From an overarching perspective, the materiality threshold is set at a high or very high severity level and a low to very high likelihood of occurrence. Further information on the IRO types, assessment perspectives and scales used can be found in the Impact materiality and Financial materiality subsections.

Revalidation and formal confirmation

As part of the iterative approach and until finalization of the report, the assessment was validated and, where required, updated based on relevant new findings or relevant new developments and events.

In total, Continental identified more than 180 IROs (PY: 150), of which 69 (PY: 75) were classified as material. The increase in assessed IROs compared with the previous year is primarily due to greater disaggregation. The lower number of material IROs is due, among other factors, to structural changes of the company resulting from the spin-off of the former Automotive and Contract Manufacturing group sectors. Further details on each material IRO can be found in the respective topic-related sections under the Material impacts, risks and opportunities subsections.

The Sustainability Steering Committee was involved in milestones of the IRO assessment, acted as a control body and formally confirmed the results. In addition, the Continental Group’s Governance, Risk and Compliance (GRC) Committee, which oversees general risk management, was indirectly involved in the process and was informed in particular about the IRO assessment and the interrelations with risk management.

Continental incorporated a range of methods and assumptions into the IRO assessment that reflect both current and projected developments, based on well-founded expert evaluations as well as insights from studies, ratings and other relevant sources. The main assumptions underlying the IRO assessment are as follows:

- Continental assumes that environmental factors and social influences will have an overall increasing influence on business activities, supply chains and market conditions, for example regarding the future availability of resources, the ecological transition and socio-economic trends.

- The financial assessment is based, among other things, on assumptions regarding future regulatory developments, market trends and technological advancements. The likely consequences of these regulatory changes were taken into account. Moreover, Continental assumes that (green) technologies will continue to advance and support sustainability initiatives.

- The assessment of impacts, risks and opportunities related to Continental’s value chain takes into account, in particular, the specific features of the respective geographical regions, industries, business activities and types of operation.

Continental’s due diligence processes play a key role in identifying, assessing and managing impacts, risks and opportunities. They are part of the management processes described in this section under Governance as well as of the management approaches in the topic-related sections. The assessment of impacts regarding human rights is supported by the due diligence processes of Continental’s responsible value chain due diligence system (RVCDDS), for example regarding actual impacts from incidents or the assessment of potential negative impacts (see in particular the topic-related Own Workforce (ESRS S1) section and Workers in the Value Chain (ESRS S2) section).

Where specific activities, business relationships, geographical locations or other factors lead to a higher assessment of the impacts, this was essentially taken into account in the description and assessment of the IROs.

Through the holistic approach of the IRO assessment, the impacts were assessed within Continental’s own operations and in the upstream and/or downstream value chains. The relevant stage of the value chain is described in the respective impacts, risks and opportunities.

As described in the methodology, the perspectives of affected stakeholders were incorporated into the assessment process by means of internal experts acting as proxies, as well as through studies and similar external information. The stakeholders’ perspectives are incorporated into the respective management approaches as described in the topic-related sections and thus also contribute to the evaluations by the internal experts who were involved in the assessment of the IROs.

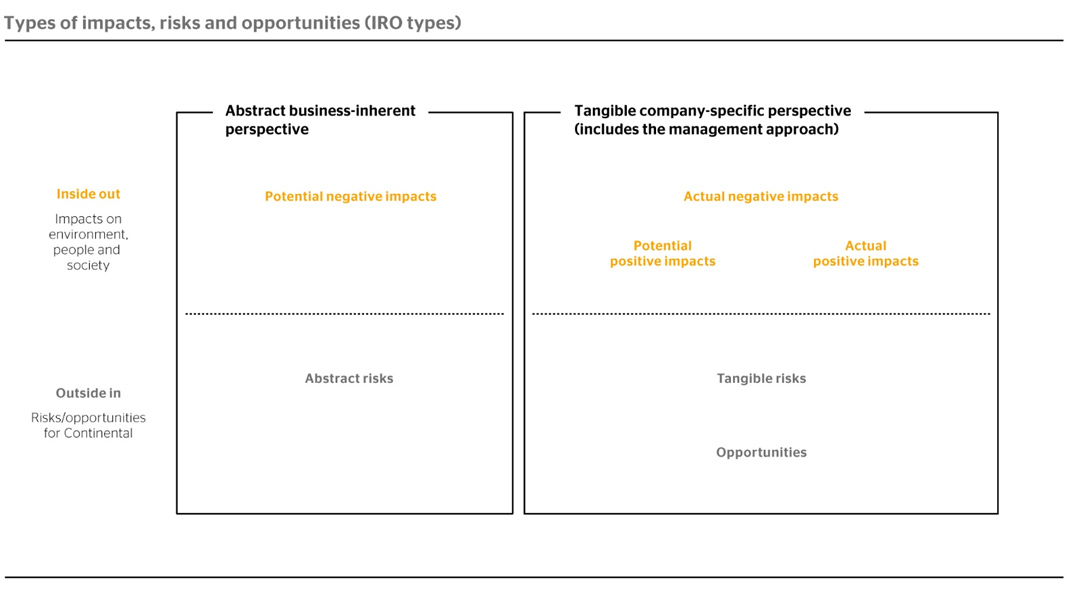

Impact materiality

For assessing impacts, Continental distinguishes between four different types of impact in accordance with the provisions set out in ESRS 1 3.4 and the operationalization derived from them:

Actual negative impact

- A material negative impact that actually occurred during the reporting year.

- The assessment is based on a tangible, company-specific perspective and includes the management approach.

- Relies on facts and figures as reference points for the assessment.

Potential negative impact

- A potential material negative impact that could occur based on inherent factors, is assumed but is not yet conclusively substantiated, or whose assessment regarding actual impacts involves significant uncertainty. Inherent factors include, for example, the type of business activity, geographical aspects, the business model or product characteristics.

- The assessment is based on an abstract, business-inherent perspective (excluding prevention and mitigation through the management approach).

Actual positive impact

- A material positive impact that actually occurred during the reporting year.

- This includes, in particular, solving a problem caused by third parties as well as having a positive influence on market standards.

- The assessment is based on a tangible, company-specific perspective and includes the management approach.

- Relies on facts and figures as reference points for the assessment.

Potential positive impact

- A material positive impact that either could occur but has not or not yet occurred, or is assumed based on the management approach pursued but is not yet substantiated.

- This includes, in particular, solving a problem caused by third parties and having a positive influence on market standards.

- The assessment is based on a tangible, company-specific perspective and includes the management approach.

Based on these definitions, Continental assumes that behind every actual impact there is a corresponding or even greater potential impact.

The impacts were assessed based on their severity or, respectively, the magnitude of the effect. For potential impacts, the likelihood was also evaluated. For both aspects, a four-point scale from “low” to “very high” was used.

The assessment of severity or, respectively, magnitude of possible effects is based on the following factors:

- the scale;

- the scope; and

- for negative impacts, also the irremediable character of the impact.

The threshold for material impacts follows the general methodology for thresholds, as laid out in this subsection under Determination of materiality.

Financial materiality

For assessing financial effects, Continental distinguishes between three different types based on the interpretation of impact types, the risk definitions used in general risk management and the provisions set out in ESRS 1 3.5:

Tangible risks

- Possible future developments that could have a material negative financial effect on Continental that is not already considered in financial planning.

- Based on tangible scenarios that take into account company-specific factors and have a tangible time horizon (short- or medium-term). The event can be clearly described, but is volatile in respect to financial effect and actual occurrence.

- The assessment is based on a tangible, company-specific perspective and includes the management approach.

Abstract risks

- Possible volatile and hard-to-predict future developments that could have a material negative financial effect on Continental that is not already considered in financial planning.

- Based on inherent factors and, for example, related possible market or regulatory trends, i.e. inherent threats, hazards and general risks that are to be mitigated.

- The assessment is based on an abstract, inherent perspective. The tangible company-specific perspective and the management approach are only partially considered, as they may not be sufficient for future developments or could be discontinued, or their effectiveness may diminish.

Opportunities

- Future developments that could have a material positive financial effect on Continental that is not already considered in financial planning.

- Based on the scenario that existing or budgeted management processes/strategies generate such a positive effect. Virtual opportunities that could theoretically be pursued but are not actively pursued do not qualify as opportunities.

- The assessment is therefore based on a tangible, company-specific perspective and includes the management approach.

Risks and opportunities were also assessed according to the level of severity or, respectively, magnitude of their possible financial effect and their likelihood of occurrence in the short, medium or long term. The financial effects were assessed using semi-quantitative guidelines that were defined in alignment with Group Risk Management. Four levels from “low” to “very high” were used as the rating scale. The financial effects considered relate to Continental’s financial position, earnings position, cash flows, access to financing, cost of capital and financial outlook. The threshold for financial materiality follows the described general methodology for thresholds, as laid out in this subsection under Determination of materiality.

The integrated approach of the IRO assessment allows Continental to assess risks and opportunities together with the topically related impacts in a combined view. This made it possible to consider interdependencies between risks or opportunities and impacts. In the topic-related sections, the detailed descriptions of impacts, risks and opportunities are grouped into related IRO clusters (e.g. all IROs on Scope 1 and Scope 2 emissions in one IRO cluster).

Integration of IROs in risk management

Group Risk Management was closely involved in all steps of the IRO assessment. Before the results were preliminarily confirmed, they were iteratively compared with the company’s risk inventory to ensure complete consistency. In this way, sustainability-related risks are integrated into the general risk management process as described below and are treated the same as risks not related to sustainability.

The IRO assessment took into account both the assessments based on the ESRS requirements and the assessments as part of the company’s risk management in accordance with the relevant requirements.

In the view of the greater differences in the required methods, the distinction between abstract and tangible perspectives was sharpened and consistency checks were carried out. Tangible sustainability-related risks were aligned and synchronized with general risk management. Impacts not directly related to an identified risk were not considered in the company’s risk management.

Further information on risk management can be found in the Report on Risks and Opportunities, in the section on Continental’s internal control and risk management system in the Main characteristics of the risk management system subsection.

The outcome of the IRO assessment confirmed the topical focus of Continental’s sustainability ambition, which is anchored in the strategy of Continental. The concrete effects of impacts, risks and opportunities on Continental’s business model, value chain, strategy and decision-making as well as how Continental responds and plans to respond to these effects are addressed in more detail in the descriptions of the IROs and in the management approaches in the respective topic-related sections.

Stakeholders and Stakeholder Engagement

Continental maintains a regular, ongoing dialogue with various stakeholders via diverse channels.

For Continental, the most important stakeholders with regard to sustainability include in particular:

- Employees and their representatives;

- Customers, consumers and end-users;

- Capital market participants;

- Policymakers;

- Affected communities and civil society;

- Actors within Continental’s supply chain; and

- Users of Continental’s sustainability reporting.

Stakeholders are involved via the following channels:

- Employees and their representatives: e.g. via works meetings, employee surveys, webcasts, meetings with employee representatives and directly via the HR departments;

- Customers, consumers and end-users: e.g. via sales departments or key account management, partnerships, trade fairs, surveys and customer service centers;

- Capital market participants: e.g. via the Annual Shareholders’ Meeting, webcasts, engagement calls and roadshows;

- Policymakers: e.g. via public affairs departments;

- Affected communities and civil society: e.g. via engagement projects and open-house events;

- Actors within Continental’s supply chain: e.g. via the purchasing departments and trade fairs;

- Users of sustainability reporting: e.g. via published sustainability reporting.

The formats used for stakeholder engagement differ depending on the stakeholder group and are organized by the respective functions to suit the individual purpose. For example, employees are involved by, among others, the HR departments.

The aim of stakeholder engagement is to bring together different perspectives, discuss any discrepancies in views and learn from each other.

The results of stakeholder engagement through various formats, along with further analyses and new ideas, are continuously incorporated into the process of further development of our sustainability strategy and reporting. In particular, the results of stakeholder engagement are taken into account in the decision-making through the management approaches described in the topic-related sections.

In the IRO assessment, an expanded understanding was created for the perspectives (including interests and views) of affected stakeholders as described in the Consideration of stakeholder interests and perspectives subsection.

Consideration of stakeholder interests and perspectives

In general, stakeholder perspectives serve as an information basis for the sustainability relevant management approaches described in the topic-related sections. At the same time, these management approaches in turn create an information basis for the overarching strategy processes with regard to stakeholder perspectives. As part of the overarching strategy processes, the described management approaches, market requirements, trends and other factors are taken into account. When changing strategy, the interests and views of stakeholders are therefore mainly included indirectly as one of many factors. Continental did not change its strategy or business models on the basis of the IRO assessment.

Continental adapts its strategy and business models as part of its strategy processes and ongoing strategic dialogue across all group sectors, as well as part of the topic-related management approaches.

Continental assumes that any change to strategy or business model has effects on the relationships to stakeholders and their perspectives – no matter whether these changes are based on sustainability-related decisions or other considerations. Continuous validation of stakeholder perspectives is therefore essential for assessing impacts, risks and opportunities as well as for subsequent strategic decision-making. Further information on strategy can be found in the Corporate Profile in the Strategy of the Continental Group section.

The identification of opportunities, particularly strategic opportunities, as part of the IRO assessment is also linked to strategy processes. The management of opportunities is described in the respective sections on management approaches of the related IRO cluster.

The perspectives and interests of affected stakeholders with regard to the company’s sustainability-related impacts were considered in the IRO assessment. The IRO assessment considering these perspectives was discussed in the Sustainability Steering Committee as well as in the Supervisory Board’s Sustainability Working Group.

Interests and perspectives of stakeholders related to own workforce

The interests, views and rights of Continental’s employees, including the respect for their human rights, are integral to shaping Continental’s strategy and business model. To incorporate their perspectives into strategic decisions, Continental is in regular exchange with employees and their representatives via various channels, such as works councils and co-determination in the Supervisory Board. Further information on the involvement of employees and their perspectives in the overall business processes can be found in the Own Workforce (ESRS S1) section. The involvement of own workforce is also described in the methodology of the IRO assessment.

Identification of Information to Be Disclosed Based on the IRO Assessment

As part of the IRO assessment, Continental allocated the identified material impacts, risks and opportunities to the corresponding ESRS sustainability matters. This sustainability report only contains information on the sustainability matters, respectively, topics, sub-topics and sub-sub-topics, that were classified as material, i.e. at least one material impact, material risk or material opportunity was identified for the respective sustainability matter. For the allocation of disclosure requirements to sustainability matters the implementation guidelines provided by the European Financial Reporting Advisory Group (EFRAG) were used as an additional source. The identified material impacts, risks and opportunities with their specific descriptions set the focus within the required disclosures, for example on own operations, the supply chain or specific product groups. The perspectives of primary users of financial reporting and other users of sustainability reporting were taken into account.

Where relevant for the understanding of specifics identified by Continental, appropriate and meaningful entity-specific disclosures were added to provide sufficient granularity of information, e.g. additional metrics used in management processes.

The principle of materiality of information was applied to calibrate the scope of information and to omit individual disclosures where they are not essential for the understanding of material impacts, risks and opportunities and the management approaches described, and are not necessary to fulfill the objectives of the corresponding disclosure requirements.

Application of Delegated Regulation (EU) 2025/1416 (“quick fix”)

When identifying the information to be disclosed for sustainability matters classified as material, Continental applies the provisions of Delegated Regulation (EU) 2025/1416 (“quick fix”) regarding the further postponement of phase-in disclosure requirements and reduced reporting on the topic areas of Biodiversity and Ecosystems (ESRS E4), Workers in the Value Chain (ESRS S2), Affected Communities (ESRS S3) and Consumers and End-Users (ESRS S4). The information disclosed in the relevant sections focuses in particular on the material aspects of the management approaches and the relevant metrics.

An overview table of the reported disclosure requirements can be found at the end of the sustainability report in the Overview and Index of Disclosure Requirements in Accordance with ESRS 2 section.

Details of Material Impacts, Risks and Opportunities

The actual and potential negative and positive impacts on environment, people and society are described in detail within the respective topic-related sections.

Many of the impacts identified are potential impacts and therefore industry-inherent, directly related to specific types of business, products, value chains or geographical regions. They can therefore be seen as impacts directly linked to Continental’s strategy and business models.

As described in the methodology of the IRO assessment, Continental used a variety of input parameters to assess the IROs, including both quantitative and qualitative data sources such as metrics, internal reports, market research and scientific studies.

Continental defined the following time intervals for potential impacts, risks and opportunities in orientation to the ESRS requirements:

- Short-term is coherent with the reporting period in the consolidated financial statements (up to one year).

- Medium-term corresponds to a period between the end of the short-term period and up to five years.

- Long-term is a period of more than five years.

As the primary time horizons Continental considers those in which the strongest impacts or effects are to be expected.

Depending on the topic, material impacts originate from own operations or from business relationships. This information can be found in the respective topic-related sections under the Material impacts, risks and opportunities subsections and, in general, in this section under the Strategy, business model and value chain subsection.

The current financial effects of the identified material risks and opportunities relating to sustainability matters include in Continental’s view in particular provisions for risks associated with the identified IROs. In particular, these are provisions for warranties (see IRO ID 64 in the Consumers and End-Users (ESRS S4) section), which amounted to a total of €30 million as of December 31, 2025 (see Note 28 of the Notes to the Consolidated Financial Statements). In addition, smaller parts of the provisions for litigation and environmental risks are linked to the risks, but mainly to the impacts from the Emissions and Substances (ESRS E2) section. Provisions for litigation and environmental risks amounted to €69 million as of December 31, 2025 (see Note 28 of the Notes to the Consolidated Financial Statements). Provisions for restructuring are only indirectly linked to the identified material risks and opportunities described in the Own Workforce (ESRS S1) section and therefore, from Continental’s perspective, do not represent current financial effects within the definitions of the ESRS.

Beyond that, no significant current financial effects on the recoverability of non-financial assets and inventories in connection with identified sustainability-related and, in particular, climate-related risks were identified.

It should be noted that current financial effects in connection with identified material risks and opportunities relating to sustainability matters are generally not independent of other associated effects.

Further information is provided in the explanations of the relevant notes to the Consolidated Financial Statements, for example in Note 28 relating to warranties. Further information on the fundamental consideration of sustainability matters in accounting are described in Note 2 of the Notes to the Consolidated Financial Statements, particularly with regard to climate-related matters in the Impact of sustainability-related and particularly climate-related matters on accounting in the reporting period subsection.

Based on the IRO assessment, taking into account the associated limitations and assumptions (as set out in the Processes to identify and assess material IROs subsection) and taking into account the management approaches, targets and key actions for target achievement reported in the topic-related sections, Continental considers its business model and strategy to be resilient. The management approaches, targets and key actions for target achievement describe Continental’s current ability to reduce its material negative impacts, increase positive impacts, manage risks and seize opportunities. Continental also assumes that these capabilities will continue to develop over time.

Further information on risk management can be found in the Report on Risks and Opportunities, in the section on Continental’s internal control and risk management system under the Main characteristics of the risk management system subsection.

The identified impacts, risks and opportunities relate to at least one sustainability matter as defined by the ESRS. The entity-specific disclosure only provides additional granularity but does not contain any new sustainability matters beyond the list of sustainability matters in ESRS 1 AR 16. The relationship between entity-specific disclosures and specific impacts, risks and opportunities is included in the description of the respective management approaches, which follow the same clustering as the impacts, risks and opportunities (IRO clusters).

The results of the IRO assessment were reported for the first time for fiscal 2024. These results served as a basis for preparing the sustainability report. In comparison to the previous year, in 2025 the methodology was refined in relation to the abstract and tangible assessment perspective with reference to ESRS 1 (see the Impact materiality and Financial materiality subsections of the Processes to Identify and Assess Material IROs section). In this context, the separate flagging of focus topics for the users of the sustainability report was removed and integrated into the assessment perspectives. Considering its limited added value, the stage “very low” was removed from the severity and likelihood rating scale. It is now merged into the stage “low”. Stakeholder involvement during the reporting year followed a two-step process with a comprehensive central review based on studies already reflecting stakeholder interests, followed by an evaluation by internal expert functions acting as proxies for stakeholders. The next review and update of material impacts, risks and opportunities will take place as scheduled in fiscal 2026.

Based on the reviews and update of the IRO assessments, as described in the Processes to Identify and Assess Material IROs section, there were no changes to materiality at the topic level. At the sub-topic level, the protection of consumer and end-user data was assessed as non-material in contrast to the previous year. This change is related to the spin-off of the former Automotive and Contract Manufacturing group sectors and their associated products and technologies. Further changes are limited to revised assessments of individual impacts, risks or opportunities. Additions, in particular, include a growth opportunity related to circular products, a potential negative impact related to freedom of association and an abstract risk related to costs associated with working conditions.

Removed items include especially a potential positive impact related to zero-tailpipe-emission vehicles and a growth opportunity related to safe mobility. For the topic of climate change adaptation, a more differentiated picture of the risk exposure emerged, in which potential asset devaluations, potential increases in operating and capital expenditure as well as potential business and supply chain interruptions are considered the material risks. At the level of individual impacts, risks and opportunities, additionally numerous detailed adjustments were made without significant topic changes, arising in particular from the revised methodology, organizational changes, updated assessments and editorial refinements.

Continental identified 69 IROs that, according to the applied methodology of the IRO assessment, were classified as material. Material IROs were identified across the supply chain, own operations and the downstream value chain. Given the different focus of topic-related sections, the distribution of IROs along the value chain varies, e.g. the Own Workforce (ESRS S1) section is, by definition, focused on own operations.

The material IROs are described in more detail in the respective Material impacts, risks and opportunities subsections of the topic-related sections in this report and can be identified with a distinct ID, as shown in the following table.Continental’s material impacts, risks and opportunities (IRO table)

Section |

IRO cluster |

ID |

Short description |

Type of IRO |

Primary |

Climate Change (ESRS E1) |

Scope 1 and |

1 |

Scope 1 and Scope 2: own emissions |

Potential negative |

Short-term |

2 |

Devaluation of assets due to climate change mitigation regulations (1.5°C scenario without overshoot) |

Abstract risk |

Medium-term |

||

3 |

Higher operating costs/investments related to climate change mitigation (1.5°C scenario without overshoot) |

Abstract risk |

Medium-term |

||

Scope 3 emissions, value chain resilience and transition |

4 |

Scope 3: emissions in the value chain (excluding use phase) |

Potential and actual negative impact |

Short-term |

|

5 |

Scope 3: emissions in the value chain (use phase) |

Potential and actual negative impact |

Short-term |

||

6 |

Higher costs for materials/services related to climate change mitigation |

Abstract risk |

Long-term |

||

7 |

Higher costs for materials/services related to climate change mitigation (1.5°C scenario without overshoot) |

Abstract risk |

Medium-term |

||

8 |

Loss of sales in connection with our portfolio and climate change |

Abstract risk |

Long-term |

||

9 |

Loss of sales in connection with our portfolio and climate change (1.5°C scenario without overshoot) |

Abstract risk |

Medium-term |

||

10 |

Growth due to climate change mitigation regulations |

Opportunity |

Long-term |

||

Climate change |

11 |

Business interruptions and higher operating costs/investments in own operations due to physical effects of climate change (SSP2 scenario) |

Abstract and |

Long-term/medium-term |

|

12 |

Business interruptions and higher operating costs/investments in own operations due to physical effects of climate change (SSP5 scenario) |

Abstract risk |

Long-term |

||

13 |

Supply chain interruptions and higher costs for materials/services due to physical effects of climate change (SSP5 scenario) |

Abstract risk |

Long-term |

||

Emissions and Substances |

Product-related |

14 |

Pollution in the use phase |

Potential negative impact |

Short-term |

15 |

Sanctions in connection with pollution in the use phase |

Abstract and |

Medium-term |

||

16 |

Loss of sales in connection with our products and pollution |

Abstract risk |

Long-term |

||

17 |

Growth due to pollution regulations |

Opportunity |

Medium-term |

||

Substances of concern and very high concern |

18 |

Negative impacts from the use of substances of concern in own operations |

Potential negative |

Short-term |

|

19 |

Negative impacts from the use of substances of concern in the supply chain |

Potential negative |

Short-term |

||

20 |

Sanctions in connection with substances of concern |

Abstract risk |

Medium-term |

||

21 |

Loss of sales in connection with our portfolio and substances of concern |

Abstract risk |

Medium-term |

||

Environmental |

22 |

Pollution by the supply chain |

Potential negative impact |

Short-term |

|

Environmental protection in own operations |

23 |

Releases or other environmental incidents in own operations |

Potential negative impact |

Short-term |

|

Biodiversity and Ecosystems |

Protection of |

24 |

Negative impacts on ecosystems due to land-use changes in the supply chain |

Potential negative |

Short-term |

25 |

Indirect negative impacts on ecosystems due to other drivers in the supply chain |

Potential negative |

Short-term |

||

26 |

Sanctions in connection with deforestation |

Abstract and |

Medium-term |

||

27 |

Supply chain interruptions and higher costs for materials/services related to deforestation |

Abstract risk |

Medium-term |

||

Biodiversity in the downstream value chain |

28 |

Negative impacts on biodiversity in the use phase and at the end of the product life cycle |

Potential negative impact |

Short-term |

|

Resource Use and Circular Economy |

Circularity |

29 |

Sourcing from primary and non-renewable sources |

Potential and actual negative impact |

Short-term |

30 |

Contribution to waste through end-of-life product treatment |

Potential and actual negative impact |

Short-term |

||

31 |

Higher costs for materials/services related to resources |

Abstract risk |

Medium-term |

||

32 |

Loss of sales in connection with our portfolio and circularity |

Abstract risk |

Long-term |

||

33 |

Growth in connection with circular products |

Opportunity |

Long-term |

||

Waste in own |

34 |

Landfill or incineration of non-recoverable waste in own operations |

Potential negative |

Short-term |

|

35 |

Waste efficiency |

Opportunity |

Medium-term |

||

Own Workforce (ESRS S1) |

Labor standards |

36 |

Negative impacts on adequate wages and fair payment |

Potential negative |

Short-term |

37 |

Negative impacts on freedom of association of own workforce |

Potential negative |

Short-term |

||

38 |

Negative impacts on employees’ working time |

Potential negative |

Short-term |

||

39 |

Negative impacts on work-life balance |

Potential negative |

Short-term |

||

40 |

Negative impacts in connection with discrimination in own operations |

Potential negative |

Short-term |

||

41 |

Negative impacts in connection with incidents of forced labor in own operations |

Potential negative |

Short-term |

||

42 |

Negative impacts in connection with incidents of child labor in own operations |

Potential negative |

Short-term |

||

43 |

Sanctions in connection with incidents related to working conditions in own operations |

Abstract and |

Medium-term |

||

44 |

Higher operating costs in connection with working conditions in own operations |

Abstract risk |

Medium-term |

||

45 |

Sanctions in connection with discrimination in own operations |

Abstract and |

Medium-term |

||

46 |

Sanctions in connection with human rights in own operations |

Abstract and |

Medium-term |

||

47 |

Loss of sales/boycott in connection with incidents related to human rights in own |

Abstract risk |

Medium-term |

||

Occupational safety |

48 |

Negative impacts on the health of own workforce |

Potential negative |

Short-term |

|

Employee privacy |

49 |

Infringement of employees’ privacy rights |

Potential negative |

Short-term |

|

Responsible |

50 |

Positive impacts on employees’ working time |

Actual and potential positive impact |

Short-term |

|

51 |

Negative impacts on secure employment |

Potential negative |

Short-term |

||

52 |

Positive impacts on secure employment |

Potential positive |

Short-term |

||

53 |

Positive impacts on social dialogue |

Potential positive |

Short-term |

||

54 |

Positive impacts on training and skill development |

Potential positive |

Short-term |

||

55 |

Business interruptions in connection with a lack of skilled workers |

Abstract and |

Medium-term |

||

Workers in the Value Chain (ESRS S2) |

Workers in the |

56 |

Negative impacts related to working conditions, equal treatment and other human rights of workers in the supply chain |

Potential negative impact |

Short-term |

57 |

Sanctions in connection with violations of labor and human rights in the supply chain |

Abstract and |

Medium-term |

||

58 |

Higher costs for materials/services in connection with human rights and working |

Abstract risk |

Medium-term |

||

Affected Communities (ESRS S3) |

Affected |

59 |

Negative impacts of own operations on affected communities |

Potential negative |

Short-term |

60 |

Negative impacts of the supply chain on affected communities |

Potential negative |

Short-term |

||

61 |

Sanctions in connection with impacts on affected communities in own operations and in the supply chain |

Abstract risk |

Medium-term |

||

Consumers and End-Users |

Technical |

62 |

Negative impacts on the personal safety of consumers |

Potential negative impact |

Short-term |

63 |

Loss of sales in connection with product safety |

Abstract risk |

Medium-term |

||

64 |

Sanctions in connection with incidents regarding product safety |

Abstract risk |

Medium-term |

||

Safe mobility |

65 |

Positive impacts on the personal safety of consumers |

Actual and potential positive impact |

Short-term |

|

Business Conduct |

Business conduct, |

66 |

Antitrust incidents in own operations |

Potential negative |

Short-term |

67 |

Negative impacts on whistleblowers |

Potential negative |

Short-term |

||

68 |

Incidents of corruption, bribery or fraud in own operations |

Potential negative |

Short-term |

||

69 |

Sanctions in connection with incidents related to business conduct |

Abstract and |

Short-term |

Specifics of the IRO Assessment for Certain Topic-Related Sections

To facilitate the comprehensiveness and robustness of the results, the IRO assessment for each topic-related section was performed following the principles and methodologies as described above. Beyond that, additional factors were taken into account for individual standards in accordance with the ESRS.

Specifics of the IRO assessment in relation to climate change

The actual negative impacts related to climate change were evaluated based on the reported GHG emissions (Scope 1, 2 and 3) of Continental’s business activities and value chain.

Regarding risks and opportunities, specific risk and opportunity scenarios were developed and evaluated as part of the IRO assessment, which are explained in the Description of methodology and assumptions subsection. The concrete scenarios are reflected in the descriptions of the respective IROs in the Climate Change (ESRS E1) section. For both, transition risks and physical risks, these include a three perspective analysis consisting of an extreme scenario, a minimal scenario and a middle pathway.

For physical risks due to climate change (see IRO ID 11, 12 and 13), the analysis was guided by selected scenarios developed by the Intergovernmental Panel on Climate Change (IPCC), which describe as key drivers an increase in extreme weather events as well as long-term climate changes (e.g. in terms of temperature) in varying degrees. In addition to a low-emission scenario (informed by SSP1‑2.6) and a middle pathway (informed by SSP3‑4.5), an extreme high-emission scenario was also assessed (informed by SSP5‑8.5).

For methodological reasons, the scenarios go beyond the considerations of general risk management and the consolidated financial statements, particularly with regard to time horizons and the abstract assessment perspective. The assessment of risks, which is included in the analysis of climate-related hazards and possibly affecting Continental’s business activities, covers own operations as well as the value chain. Because of the high uncertainty of long-term climate projections and the potentially global distribution of climate hazards, no direct analysis was performed at the level of individual locations. Instead, the assessment was performed at a macro level, focusing on the overall potential exposure of Continental and its value chain, based on the fundamental development of climate hazards in the different scenarios and structural factors such as distribution of locations on country level, specific supply chain structure or process-related features of the business activity. Among other aspects, the assessment drew on expert evaluations regarding possible effects on remaining carrying amounts over the considered time horizon. The climate-related hazards considered in the scenarios include, in particular, the increase in extreme weather events and long-term changes in climate patterns, for example in terms of temperature. From Continental’s perspective, the selected scenarios therefore address the relevant drivers of risks and opportunities and thereby also cover the relevant scenarios in the meaning of the ESRS.

The exposure and sensitivity of assets and business activities to the identified climate-related hazards were assessed semi-qualitatively under this approach. The exposure and sensitivity in connection with the identified related financial effects of the material risks are reflected in the descriptions of the associated risks in the Climate Change (ESRS E1) section under the Climate change adaptation IRO cluster. By integrating the scenario analysis into the IRO assessment, the same rating scales and time horizons were used. For methodological reasons, the standardized time horizons of the IRO assessment do not directly correspond to the different expected lifetimes of Continental’s assets. The “short-term” and “medium-term” levels in the IRO assessment essentially correspond to the time horizons of the financial annual and long-term planning. This methodological difference does not materially affect the risk assessment. The assessment is aligned with general risk management. Further information on the time horizon of long-term planning can be found, for example, in the disclosures on impairment losses in Note 2 of the Notes to the Consolidated Financial Statements. In addition, further information on the consideration of climate-related matters in accounting, if relevant and material, can be found in Note 2 of the Notes to the Consolidated Financial Statements in the Estimates subsection under Impact of sustainability-related and particularly climate-related matters on accounting in the reporting period.

For transition risks (see IRO ID 2, 3, 6, 7, 8 and 9), the scenarios developed by the International Energy Agency (IEA) were used as a guidance, which describe macroeconomic transitional changes, particularly regarding regulation and market developments, in varying degrees. The minimal scenario was formulated and assessed using the Stated Policies Scenario (STEPS), while the middle-pathway scenario used the Announced Pledges Scenario (APS). The extreme scenario (1.5°C without overshoot) is derived from the scenario requirement in ESRS E1 20c(i), which mandates at least a scenario of a 1.5°C pathway with no or limited overshoot. All scenarios include increasing regulation, but in case of no or only a limited overshoot of 1.5°C being allowed, it was assumed considering current forecasts that full carbon neutrality of the global economy would be achieved already in the medium term.

The exposure and sensitivity of assets and business activities to the identified abstract transition risks were assessed semi-qualitatively in the IRO assessment. By applying the IRO methodology, the assumptions regarding the probability, extent and duration of the transition events were taken into account. The IRO assessment concluded that Continental’s assets, business activities and product portfolio are fundamentally capable of transition and do not lead to any significant, tangible transition risks, but rather only to a general, abstract risk exposure that is inherent to the industry. The financial effects of the abstract transition risks are reflected in the descriptions of the associated risks in the Climate Change (ESRS E1) section. Due to the integration into the IRO assessment, the same time horizons apply.

Specifics of the IRO assessment in relation to pollution

The identification and assessment of potential and actual impacts, risks and opportunities in relation to pollution in own operations, the supply chain and the downstream value chain included a screening of Continental’s locations and business activities under consideration of the respective management approaches as well as the related metrics. The identification and assessment were integrated into the impact, risk and opportunity assessment following the described methodology. The assessment was also compared with external data sources.

Continental took into account the perspective of affected communities regarding pollution by aligning the assessments with proxies from internal functions who represented their interests and by comparisons with external information sources. The information received was taken into account in the development of the respective management approaches, in particular for own operations. There was no direct consultation with affected communities.

Specifics of the IRO assessment in relation to water and marine resources

The identification and assessment of potential and actual impacts, risks and opportunities regarding water and marine resources related to own operations, the supply chain and the downstream value chain included a screening of Continental’s locations and business activities under consideration of the respective management approaches as well as the related metrics. The identification and assessment were integrated into the impact, risk and opportunity assessment following the described methodology. The assessment was also compared with external data sources and revealed that there are no material IROs for this sustainability matter.

Aspects relating to water pollution were considered as part of the IRO assessment under the topic of pollution.

Continental took into account the perspective of affected communities regarding water and marine resources by aligning the assessments with proxies from internal functions who represented their interests and by comparisons with external information sources. There was no direct consultation with affected communities.

Specifics of the IRO assessment in relation to resource use and circular economy

The identification and assessment of potential and actual impacts, risks and opportunities related to resource use and circular economy, in particular regarding resource inflows, resource outflows and waste in Continental’s own operations, in the supply chain and in the downstream value chain, included a screening of Continental’s locations in relation to waste and business activities, among other aspects regarding products and materials purchased by Continental. The identification and assessment took into account information from the respective management approaches as well as related metrics. The identification and assessment were integrated into the impact, risk and opportunity assessment following the described methodology.

Continental took into account the perspective of affected communities regarding resource use and circular economy by aligning the assessments with proxies from internal functions who represented their interests and by comparisons with external information sources. The information received was taken into account in the development of the respective management approaches, in particular for own operations. There was no direct consultation with affected communities.

Specifics of the IRO assessment in relation to business conduct

The identification and assessment of potential and actual impacts, risks and opportunities regarding business conduct included, in particular, the consideration of Continental’s types of business activities, geographies, industries and types of transactions as well as the respective management approaches and associated metrics.

Governance

Administrative, management and supervisory bodies

The Executive Board of Continental AG manages the company independently and in the best interests of the enterprise. All members of the Executive Board jointly bear responsibility for managing the company. Regardless of this principle of joint overall responsibility, each Executive Board member is individually responsible for the Executive Board function entrusted. At the end of the reporting year, the Executive Board consisted of five members. With the turn of the year, the board was reduced to four members, as the former chairman stepped down from the Executive Board by mutual agreement as part of Continental’s realignment.

The Executive Board is supported by the Group Sustainability group function in sustainability management, the preparation of the sustainability report and reporting to the Supervisory Board.

Continental’s Supervisory Board is responsible for appointing the members of the Executive Board, as well as for supervising and advising the Executive Board in its management of the company. This includes, in particular, issues such as strategy, planning, business development, risk exposure, risk management, compliance and the accuracy of financial and sustainability reporting.

The Supervisory Board regularly addresses sustainability matters. In addition, it has established a Sustainability Working Group that specifically addresses sustainability matters relevant for Continental on a regular basis. The working group consists of two shareholder representatives and two employee representatives. All members have relevant specialist knowledge. Furthermore, sustainability reporting, sustainability-related risk management, the related internal control system as well sustainability-related compliance management systems are regularly addressed by the Audit Committee of the Supervisory Board.

The Supervisory Board is composed in accordance with the German Co-determination Act (Mitbestimmungsgesetz – MitbestG) and the company’s Articles of Incorporation. Half the members of the Supervisory Board are elected by the shareholders in the Annual Shareholders’ Meeting (shareholder representatives), while the other half are elected by the employees of Continental AG and its German subsidiaries (employee representatives).

Before September 5, 2025, the Supervisory Board had 20 members. In connection with the spin-off of the former Automotive and Contract Manufacturing group sectors on September 17, 2025, the three Supervisory Board’s employee representatives who had employment contracts with spun-off companies were required by law to step down from the Supervisory Board. In addition, the representatives of the IG Metall labor union (two members) and two shareholder representatives resigned from their positions in September 2025. Five new members were appointed to the Supervisory Board by judicial appointment on September 22, 2025. The Supervisory Board has since comprised 18 members.

In accordance with recommendation C.1 of the German Corporate Governance Code, the Supervisory Board has specified objectives for its composition and developed a profile of skills and expertise covering, among other things, sustainability matters, particularly in the areas of environment and social responsibility.

Furthermore, the Executive Board and the Supervisory Board are expanding their sustainability-related expertise through regular participation in different exchange formats on developments regarding sustainability in their area of responsibility, and in close consultation with sustainability experts within and outside the organization. In addition, in the reporting year, an intensive voluntary training on sustainability regulations was conducted for the Supervisory Board.

Through this continuous exchange on sustainability matters, the skills and specialist knowledge of the administrative, management and supervisory bodies are adequate to manage material impacts, risks and opportunities.

The Supervisory Board members collectively cover all skills, expertise and experience deemed to be significant in view of Continental’s business activities. These include in particular:

- Corporate governance;

- Sector- and company-specific experience;

- International experience;

- Sustainability;

- Risk management and reporting.

In addition, this enables the company to provide newly elected members of the Supervisory Board with a comprehensive overview of the company’s products and technologies as well as of finance, controlling, corporate governance and sustainability at Continental.

All Executive Board members have experience relevant to Continental’s sectors, products and geographical locations as well as further expertise that is relevant for their responsibilities. These criteria are, among other aspects, also part of the internal succession planning for management positions.

Further information on the Executive Board and Supervisory Board, such as on the expertise of the individual Supervisory Board members, can be found in the Corporate Governance Statement. In addition, further information on the individual members of the Executive Board and Supervisory Board can also be found on our website under Company/Corporate Governance.| Metrics for the composition of administrative, management and supervisory bodies (as of December 31) | 2025 |

2024 |

| Number of executive members (Executive Board) | 5 |

6 |

| Number of non-executive members (Supervisory Board) | 18 |

20 |

|

|

|

| Gender distribution, in % |

|

|

| Male | 65 |

73 |

| Female | 35 |

27 |

|

|

|

| Independent members of the Continental Supervisory Board, in % | 100 |

100 |

Definitions, assumptions and calculation methods:

General information

- - The management and supervisory bodies are the Supervisory Board and the Executive Board of Continental AG.

- - The composition of the management and supervisory bodies as of December 31, 2025, is taken into account.

- - The executive members of Continental management are the members of the Executive Board. The non-executive members are the members of the Supervisory Board.

Gender distribution

- - The gender distribution of the Executive Board is based on the information specifically documented in Continental’s systems. This information therefore represents Continental’s state of knowledge, taking into account local legislation and co-determination.

- The gender distribution of the Supervisory Board is based on the information provided in their own résumés, which are published on Continental’s website.

- - As of December 31, 2025, the ratio of female to male members of the management and supervisory bodies is 8 to 15.

Independent members of the Continental Supervisory Board

- - The independence of a Supervisory Board member is defined in accordance with recommendation C.7 the German Corporate Governance Code (Deutscher Corporate Governance Kodex – DCGK).

- - Taking into account the ownership structure, a Supervisory Board member is to be considered independent in the context of this metric if they are independent of the company and its Executive Board. In accordance with the DCGK, only shareholder representatives must prove their independence. Consequently, only the shareholder representatives are included in this metric.

Roles and responsibilities

Oversight of sustainability follows a staggered approach through regular meetings with a predefined agenda and, where applicable, adoption of resolutions. The structure is as follows:

- The Group Sustainability group function and operational sustainability governance are overseen by the Sustainability Steering Committee, in which the entire Executive Board is represented.

- Oversight of the Executive Board is exercised by the Supervisory Board.

Since July 2025, as part of the company’s restructuring, the Group Sustainability group function reports directly to the chairman of the Executive Board. Previously, it reported directly to the Executive Board member responsible for Group Human Relations (director of Labor Relations) and Group Sustainability.

Ultimate responsibility for the management, monitoring and oversight of impacts, risks and opportunities in the area of sustainability lies with the Executive Board. Operational tasks, particularly in relation to sustainability governance and reporting, are assigned to Group Sustainability. The Tires and ContiTech group sectors also have their own operational sustainability departments.

Sustainability management within the Continental Group is regulated by a dedicated sustainability rule. Six administrative, management and supervisory bodies are responsible for monitoring Continental’s impacts, risks and opportunities:

- Supervisory Board:

The Supervisory Board is responsible for overseeing the integration of sustainability matters into the business strategy and corporate planning. This includes the composition of the Executive Board (including responsibility for sustainability), the integration of sustainability into the remuneration system of the Executive Board as well as the assessment of sustainability reporting. - Audit Committee of the Supervisory Board:

The Audit Committee addresses sustainability in relation to the monitoring of accounting processes, including processes for sustainability reporting. - Sustainability Working Group of the Supervisory Board:

The Sustainability Working Group established by the Supervisory Board deals with sustainability matters relevant to Continental. The working group includes two shareholder representatives and two employee representatives. - Executive Board:

The Executive Board of Continental AG has overall responsibility for sustainability. Important strategic decisions regarding sustainability with significant group relevance are made by the Executive Board, along with regular reviews and, if necessary, updates of the sustainability ambition, by systematically considering sustainability-related impacts, risks and opportunities. - Sustainability Steering Committee:

The Sustainability Steering Committee established by the Executive Board assumes the role of primary steering and decision body for sustainability at group level. Its tasks include: - Reviewing and confirming the assessment of material impacts, risks and opportunities;

- Defining the group-wide sustainability strategy, public sustainability targets and corresponding key actions;

- Defining the group-wide sustainability metrics that go beyond legal requirements.

- Group Sustainability:

The Group Sustainability group function holds operational responsibility for the sustainability framework at group level, in close collaboration with other functions. Its main tasks include complying with sustainability regulations and steering of the sustainability governance and reporting, including the IRO assessment.

Further roles regarding sustainability are defined by the sustainability governance framework, such as the operational sustainability departments at group sector level.

The following documents regulate the roles and responsibilities regarding sustainability-related topics, including the assessment of impacts, risks and opportunities. Most of these documents are not exclusively focused on sustainability, but are relevant for its management:

- German Stock Corporation Act (Aktiengesetz – AktG) (including the duties, constitution and due diligence obligations of the Executive Board and Supervisory Board)

- Articles of Incorporation of Continental AG

- By-Laws of the Executive Board (including in the annex to the business organization plan regarding the areas of responsibility of the members of the Executive Board, including sustainability)

- By-Laws of the Supervisory Board (internal rules of procedure of the Supervisory Board, governing in particular the reporting of the Executive Board to the Supervisory Board on sustainability issues)

- Continental sustainability rules (regarding sustainability governance within the Continental Group)

Sustainability targets are set to address material impacts, risks and opportunities and to achieve Continental’s sustainability ambition. Public sustainability targets for the Continental Group are approved by the Sustainability Steering Committee.

The responsibility of the Sustainability Steering Committee also includes adapting and further developing these targets.

The public sustainability targets are set and adopted together with the key actions and the corresponding metrics to measure progress. The metrics are published in the sustainability reporting and are regularly monitored by the Sustainability Steering Committee.

Consideration of sustainability matters in corporate supervision

Group Sustainability is responsible for regularly providing the administrative, management and supervisory bodies with appropriate information on the results of assessing material impacts, risks and opportunities of sustainability matters and their implications, in accordance with the described governance structure.

Continental’s business strategy and risk minimization measures are aligned with the identified material impacts, risks and opportunities, as described in the respective management approaches. Where relevant, trade-offs between various impacts, risks and opportunities are taken into account in the strategic processes.