The goal is the sustained increase in the Continental Group’s value.

Value management

Value management at Continental is focused on value creation through profitable sales growth. The most significant financial performance indicators are sales, the adjusted EBIT margin, capital expenditure and adjusted free cash flow. For management purposes and to map interdependencies, we use key figures based on these financial performance indicators.

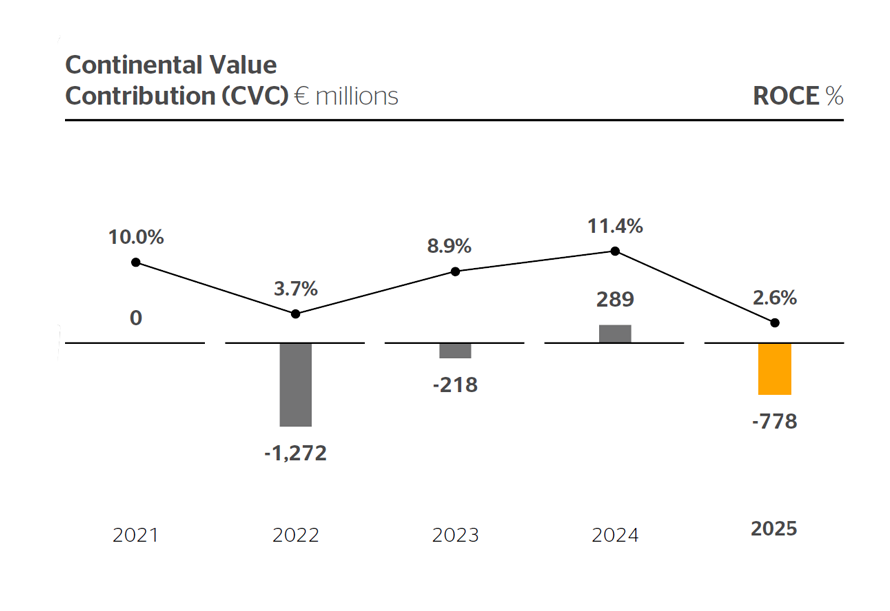

Another key figure as part of the value-driver system is return on capital employed. Our mid-term corporate objectives center on the sustainable enhancement of the value of each individual operating unit. This goal is achieved by generating a positive return on the capital employed that sustainably exceeds the associated equity and debt financing costs within each individual unit. Crucial to this is that the absolute contribution to value (the Continental Value Contribution (CVC)) increases year-on-year. This can be achieved by increasing the return on capital employed (with the costs of capital remaining constant), lowering the costs of capital (while maintaining the return on capital employed) or decreasing capital employed over time. The performance indicators used are earnings before income and tax (EBIT), capital employed and the weighted average cost of capital (WACC), which is calculated from the proportional weight of equity and debt costs.

Continental Value Contribution (CVC) in € millions / ROCE in % (For 2025, the figures for continuing operations are shown.)

EBIT is the net total of sales, other income and expenses plus income from equity-accounted investees and from investments but before financial result and income tax expense. In the year under review, EBIT for continuing operations was €272 million.

Capital employed is the funds used by the company to generate its sales. At Continental, this figure is calculated as the average of operating assets as at the end of the quarterly reporting periods. In 2025, average operating assets for continuing operations amounted to €10.5 billion.

The return on capital employed (ROCE) represents the ratio of these two calculated values. Comparing a figure from the statement of income (EBIT) with one from the statement of financial position (capital employed) produces an integral analysis. We deal with the problem of the different periods of analysis by calculating the capital employed as an average figure over the ends of quarterly reporting periods. The ROCE for continuing operations amounted to 2.6% in 2025.

The WACC is calculated to determine the cost of financing the capital employed. Equity costs are based on the return from a risk-free alternative investment plus a market risk premium, taking into account Continental’s specific risk. Borrowing costs are calculated based on Continental’s weighted debt-capital cost rate. Based on the long-term average, the cost of capital for our company is about 10%.

Value is added if the ROCE exceeds the WACC. We call this value added, produced by subtracting the WACC from the ROCE multiplied by average operating assets, the Continental Value Contribution (CVC). In 2025, the CVC for continuing operations amounted to ‑€778 million.

EBIT, the ROCE and the CVC in 2025 were influenced in particular by special effects resulting from the spin-off of the former Automotive and Contract Manufacturing group sectors and the valuation of the OESL disposal group.

| ROCE by group sector (%) | ||||

|---|---|---|---|---|

| 2025 | 2024 continuing operations | 2024 continuing and discontinued operations | ||

| Tires | 23.3 | 24.9 | 24.9 | |

| ContiTech | ‑20.6 | 8.1 | 8.2 | |

| Automotive | — | — | 2.6 | |

| Contract Manufacturing | — | — | 12.6 | |

| Continental Group | 2.6 | 19.4 | 11.4 | |

Financing strategy

Our financing strategy aims to support the value-adding growth of the Continental Group while at the same time complying with an equity and liabilities structure adequate for the risks and rewards of our business.

The Finance & Treasury group function provides the necessary financial framework to finance corporate growth and secure the long-term existence of the company. The company’s annual investment requirements are likely to be around 6% to 7% of sales in the coming years.

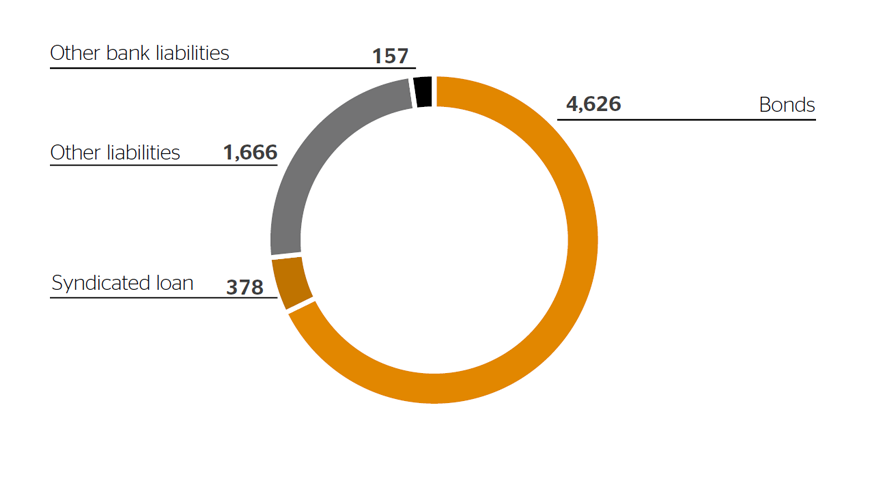

Composition of gross indebtedness (€6,826 million)

Our goal is to finance ongoing investment requirements from the operating cash flow. Other investment projects, such as major acquisitions, should be financed from a balanced mix of equity and debt depending on the debt ratio and the liquidity situation to achieve constant improvement in the respective capital market environment. In general, the ratio of net indebtedness to EBITDA over the past 12 months (leverage ratio) should be less than or equal to 1 in the medium term. If justified by extraordinary financing reasons or specific market circumstances, we can rise above this ratio under certain conditions. The leverage ratio has been reported in place of the gearing ratio as a new key figure for assessing the financing structure since mid‑2025, since it reflects the relationship between debt and profitability, making it a more suitable performance indicator in Continental’s opinion. The leverage ratio is also considered to be more relevant in capital market communication. The leverage ratio as at December 31, 2025, was 2.8. Another key figure of capital management is the equity ratio. It should exceed 30% in the medium term and amounted to 23.4% at the end of 2025.

Gross indebtedness amounted to €6,826 million as at December 31, 2025. Key financing instruments are the syndicated loan, adjusted in 2025, with a revolving credit line of €2.5 billion that has been granted until December 2027, and bonds issued on the capital market. Our gross indebtedness should be a balanced mix of liabilities to banks and other sources of financing on the capital market. For short-term financing in particular, we use a wide range of financing instruments. As at the end of 2025, this mix consisted of bonds (68%), the syndicated loan (6%), other bank liabilities (2%) and other indebtedness (24%), based on gross indebtedness.

The syndicated loan was renewed ahead of schedule in December 2019. It consisted of a revolving tranche of €4.0 billion and had an original term of five years. As a result of exercising two options, each extending the term of the loan by one year, this financing commitment was ensured until December 2026. In the first half of 2025, the following amendments were agreed: Firstly, the term was extended by an additional year until December 2027, although one bank – with a share of €90 million – did not participate in the extension and will withdraw from the syndicated loan in December 2026. Secondly, it was agreed that the volume would be reduced upon completion of the spin-off of the former Automotive and Contract Manufacturing group sectors in September 2025. Since September 17, 2025, the volume of the syndicated loan has stood at €2.5 billion. Furthermore, its margin is no longer linked to the Continental Group’s sustainability performance.

The company aims to have at its disposal unrestricted cash and cash equivalents of around €1.0 billion. These are supplemented by committed, unutilized credit lines from banks in order to cover liquidity requirements at all times. These requirements fluctuate during a calendar year, owing in particular to the seasonal nature of some business areas. Unrestricted cash and cash equivalents amounted to €1,424 million as at December 31, 2025. There were also committed and unutilized credit lines of €2,733 million.

As at December 31, 2025, €378 million of the revolving credit line of €2.5 billion had been utilized. Around 68% of gross indebtedness is financed on the capital market in the form of bonds. The interest coupons vary between 2.500% and 4.000% p.a. In 2025, Continental redeemed a maturing bond in the amount of €600 million. In conjunction with this, and in order to optimize the maturity profile of its indebtedness, Continental issued two new bonds in 2025. These bonds, one with a volume of €750 million and term of three and a half years and the other with a volume of €600 million and a term of three years and nine months, were both placed with investors at an interest rate of 2.875% p.a. In addition to the forms of financing already mentioned, there were also bilateral credit lines with various banks in the amount of €769 million as at December 31, 2025. Continental’s corporate financing instruments currently also include sale-of-receivables programs and commercial paper programs. As in the previous year, Continental primarily had two commercial paper programs in 2025: in Germany and in the USA. At the end of 2025, the program in Germany had been utilized in the nominal amount of €630 million, and the program in the USA in the nominal amount of €51 million.

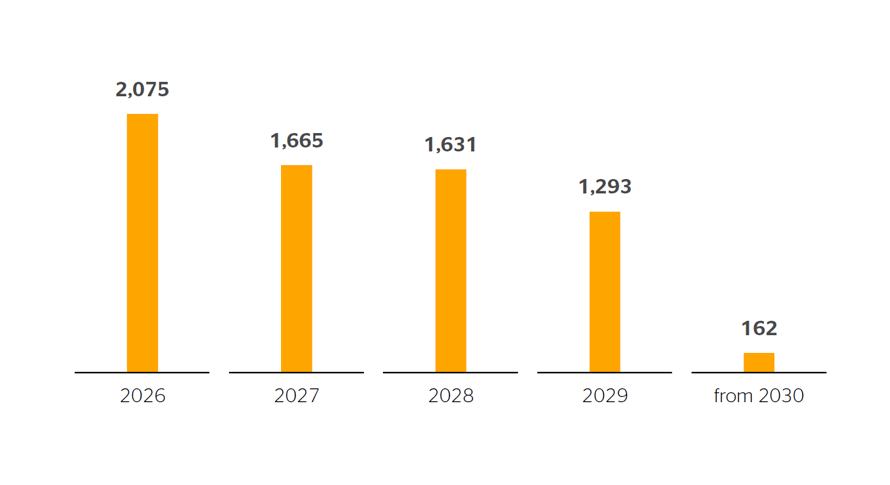

Maturity profile

Continental strives for a balanced maturity profile, particularly with respect to its capital market liabilities, in order to be able to repay the amounts due each year from free cash flow as far as possible. Aside from short-term indebtedness, most of which can be rolled on to the next year, one bond in the amount of €750 million will mature in 2026. The other bonds issued since 2022 require repayments of €1,125 million in 2027, €1,500 million in 2028 and €1,200 million in 2029.

Maturities of gross indebtedness (€6,826 million)

Continental’s credit rating unchanged

In the reporting period, Continental AG was rated by the three credit rating agencies Standard & Poor’s, Fitch and Moody’s, each of which maintained their investment-grade credit ratings in 2025. In May 2025, the rating outlook at Standard & Poor’s changed from developing to stable. The most recent rating adjustment took place in spring 2020, when all three credit rating agencies adjusted their long-term credit rating downward by one notch. Our goal in the medium term is a credit rating of BBB+.

| Credit rating for Continental AG | ||

|---|---|---|

| December 31, 2025 | December 31, 2024 | |

| Standard & Poor’s1 | ||

| Long-term | BBB | BBB |

| Short-term | A-2 | A-2 |

| Outlook | stable | developing |

| Fitch2 | ||

| Long-term | BBB | BBB |

| Short-term | F2 | F2 |

| Outlook | positive | positive |

| Moody’s3 | ||

| Long-term | Baa2 | Baa2 |

| Short-term | P-2 | P-2 |

| Outlook | stable | stable |

1 Contracted rating since May 19, 2000.

2 Contracted rating since November 7, 2013.

3 Contracted rating since January 1, 2019.